Projets 3: Portfolio Optimization

Modern Portfolio Theory

It was formulated in the 1950 by Harry Markowitz.

what is the main idea?

A single stock is quite unpredictable or risky: we do not know for certain whether a stock will go up or down.

But we may combine several stocks, in order to reduce risk as much as possible. DIVERSIFICATION.

when a given value of stock goes down another goes up. Combining assets is the main idea: it is the same as the black-scholes Model.

The model has some Assumptions: * the return are normally distributed: with mean (u) and variance(sigma) * the investors are risk-averse: inverstor will take more risk if the are excepting more rewards low –> low return higher risk –> higher return

With modern portfolio theory, investors can construct optimal portfolios offering the maximum possible expected return for a given level of risk!!

so what is an efficient portfolio?

It is a portfolio that has the highest rewards for a given level of risk.

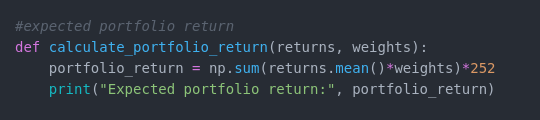

How to calculate the return of an asset ?

daily return plot:

Wi is the weight of the i stock.

ri the return of the i stock // calculate on its historical data

Ui the expected return of the portfolio

portfolio return formula:

this model relies on historical data. Historical Data mean performance is assumed to be the best estimator for future performance.

what about the risk of the portfolio ?

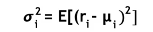

the risk has something to do with volatility, volatility has something to do with the standard deviation

covariance meaure how much 2 point(or stocks ij) vary together

covariance formula

covariance_form ..> negative covariance means returns move inversely ..> positie covariance means returns move together

Markowitz’s theory is about diversification: possessing assets(stocks) with high positive covariance does not provide very much diversification!!!.

the aim of diversification is to eliminate fluctuations in the long term. So uncorrelated stocks are better!!

variance formula

for calculating the variance of the portfolio we need the covariance matrix cointaining all the covariances of the stocks involved in the portfolio.

variance portfolio

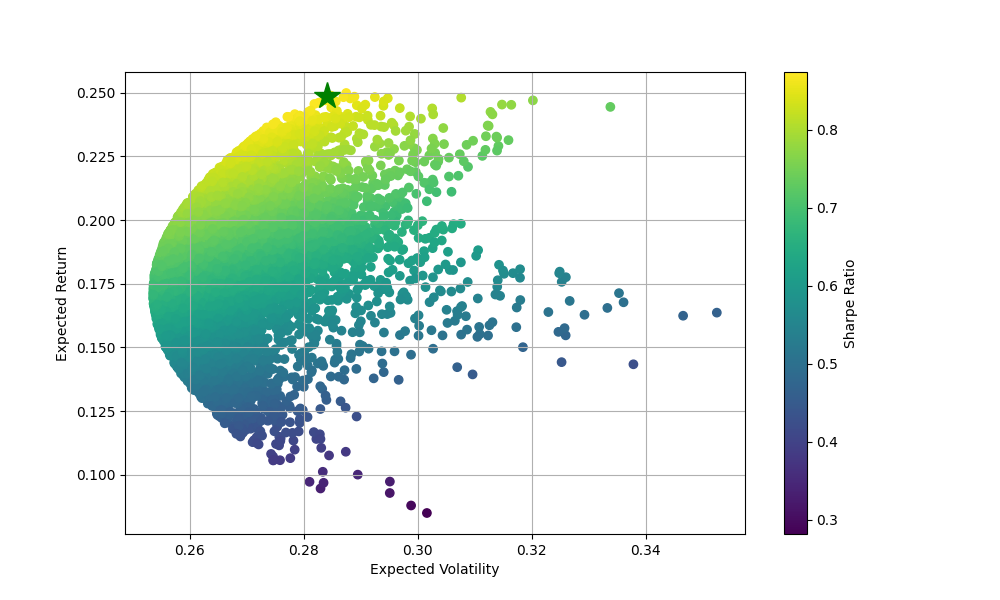

Efficient Frontier

every dots in the plot represent w (weight) –> so different portfolios or set of portolio An investor is interested in : 1. the maximum return given a fixed risk level 2. minimum risk given a fixed return

these portfolio make up the so called efficient-frontier!!! this is the main feature of Markowitz model: the investor can decide the risk or the expected return

–> basic rule: if you want to make money, you have to take risk!!!

What is Shape Ratio ?

it is one of the most important risk/return measures used in finance –> it describes how much excess return you are receiving for extra volatility that you endure holding a riskier asset(stock) a sharpe-ratio S(x)>1 is considered to be good.

sharpe-ratio formula

Capital allocation line:

The optimal portfolio lie on the capital allocation line if the portfolio can containe stocks as well as risk-free rate(bond) if you dont want to take risk you will be on the risk-free point that contain zero risk.

IMPLEMENTATION IN PYTHON

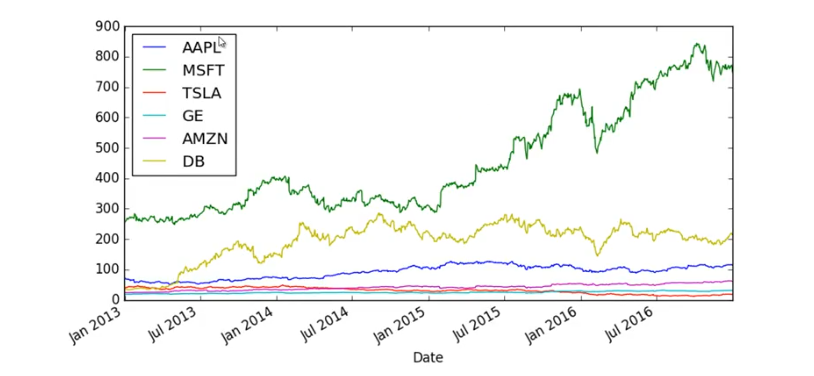

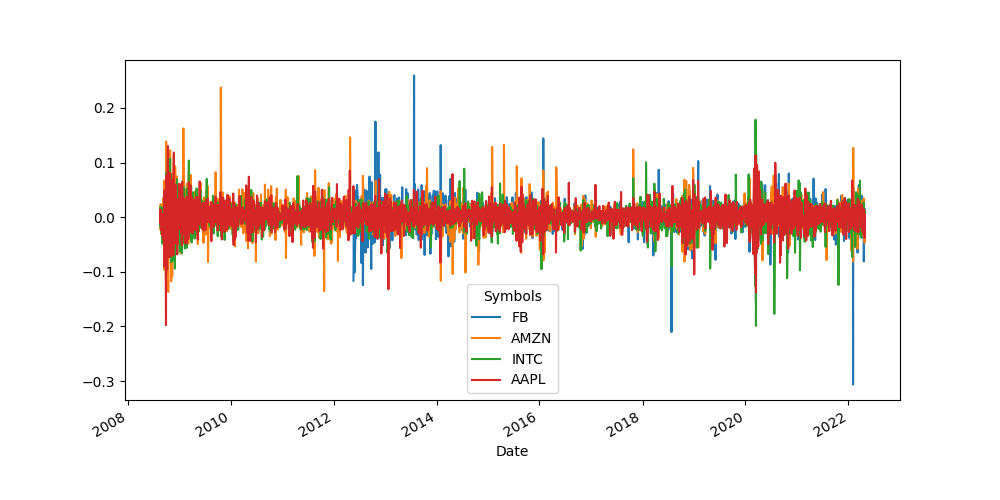

Returns of each stock since 13 years:

See how stocks are correlated to each other:

See the expected portolio return and the expected portolio volatility:

result:

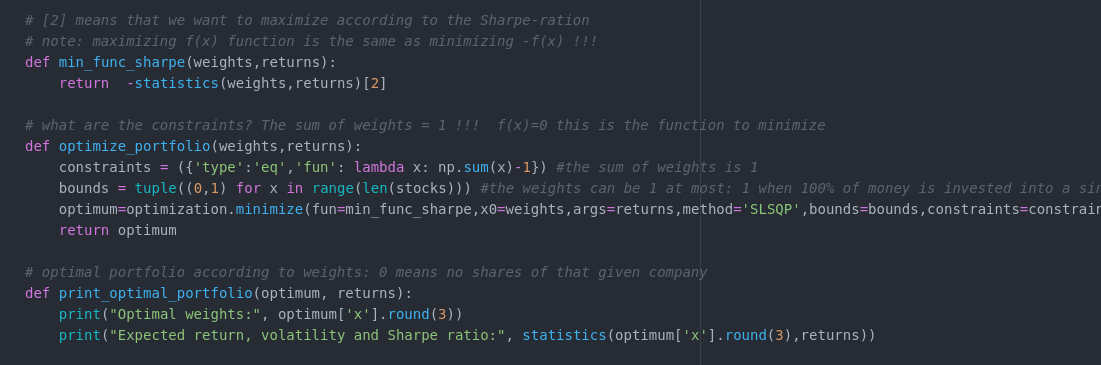

See the optimal portolio weights:

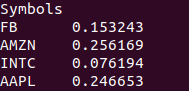

FB AMZN INTC AAPL

Optimal weights: [0.017 0.376 0. 0.607]

this mean that we need to attribuate 1.7%, 37.6%, 0%, and 60.7% resspectively to FB, AMZN, INTC, and AAPL of our wealth or capital. Only invest in FB, AMZN, and AAPL. invest in INTC will not give us a reward.

Optimal Portfolio:

Expected return = 0.24864315 volatility = 0.28413197 Max Sharpe ratio = 0.87509743

Conclusion:

The main ideal of this theory is combine several stocks, in order to reduce risk as much as possible. DIVERSIFICATION. The goal of investor is to get rewards with less risks, or no risks. But combine several stocks, dont reduce all the risks. It reduce only the unsystematic risk, risk that is specific to the company itself. CAPM(Capital Asset Pricing Model) describes the relationship between systematic risk and expected return for assets, particularly stocks. It say that if we want to reduce risk, we need to take into account the market risk (inflation, war, recesion…). The variation of stock prices has some relationship with the market. Derivative instruments can be used to reduce or eliminate all the risks, with a good strategy.